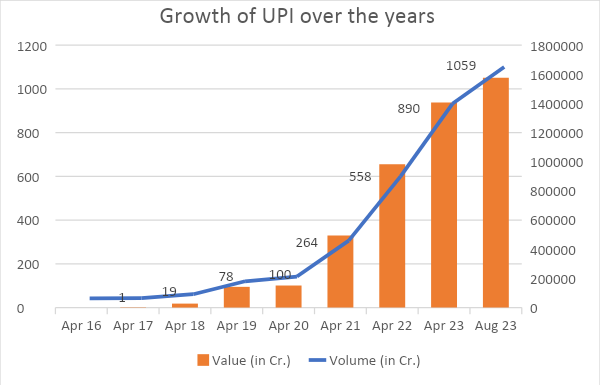

Exactly seven years ago, there were 25 banks live on UPI, with a transaction value of Rs 32.64 crores on the interface during September 2016. Fast forward to September 2023, and the monthly transaction value stood at Rs 15.79 lakh crores! Even the number of banks live on UPI has now increased to 492.

Unified Payments Interface (UPI) was introduced by the National Payments Corporation of India (NPCI) as a smartphone application to transfer money between bank accounts. In UPI you get several banking features, and options like merchant payment, fund transfer, peer-to-peer collection request, etc.

UPI was launched in 2016 as a one-stop platform for digital payments in India. The demonetisation of Rs 500 and Rs 1000 currency notes later that year became a watershed moment in the interface’s history. With people starting to use digital payment more as a compulsion than a preference, digital payments in India blossomed. Within six months of demonetisation, the transaction volume on UPI rose from a meagre Rs 29 lakhs to Rs 7.2 crores.

Making things easier was the sudden availability of affordable internet in India. Jio Telecom became available to the public in September 2023, which started a price war in the telecom sector for data packs. Thus, circumstances and technology aligned rather perfectly for UPI in 2016. And it has been on an ascendancy ever since.

UPI has made fund transfers streamlined and hassle-free with its all-encompassing digital payments ecosystem. It has also improved the digital payment user experience remarkably. The rise of UPI in India is best explained by these popular advantages –

Fast transaction – Just complete a quick registration process and you can make a UPI payment that gets reflected in the receiver’s account almost instantly. It’s perfect for on-the-go transactions like at a tea stall or a vegetable cart. The mobile-first design allows fast push and pull payments and can be easily identified with the common UPI identifier.

Go cashless – With the widespread presence of UPI, it is now easier to go cashless. No need to look around for loose changes over a photocopy when you can pay Rs 3 online. UPI allows bank transfers, peer-to-peer and merchant transfers. This means that leaving your home without carrying cash is less likely to get you stranded these days. Besides, the risk of theft or misplacing of physical cash is eliminated.

Cash usage percentage out of the total point of sale transaction value in India – 71% in 2019; 27% in 2022

Wide choices – UPI acts as a single platform that allows linking with multiple bank accounts. So, if you have more than one bank account you can link all or some of them onto your UPI mobile app. Accordingly, you can choose which bank account to pay from while making the next online payment.

Secure transactions – UPI eliminates the need to expose bank credentials on every online transaction. Bank account details once entered into the UPI app enable you to make and receive as many payments as you want. The app itself is protected with very simple, single-click, two-factor authentication requiring PIN and/or biometric protocols.

Return gifts – In a cash economy, getting something back from the expenses made is almost unthinkable. UPI platforms, on the other hand, offer various rewards, discounts and cashback against payments.

While the domestic popularity of UPI is well-documented, international acceptance has also started coming in. International acceptance is made possible through arrangements between the payment operators of two countries. UPI gained much-published acceptance in France and Singapore. Other overseas markets that have started to accept UPI payments include Malaysia, UAE, the UK, Nepal, and the Benelux countries.

At the helm of these international tie-ups is the NPCI subsidiary, NPCI International Payments Limited (NIPL). NIPL is entering into agreements with countries and building the acceptability of RuPay and UPI further. For many countries, particularly developing ones, the cash circulation is very high. Replacing it with POS machines can be an expensive affair. With UPI, India offers these countries an affordable alternative.

Global Fintech Fest Highlights - NCPI further expanded the UPI service suite with the launch of the credit line on UPI, UPI LITE X, Tap & Pay, Hello UPI, and BillPay Connect. It was the highlight of the RBI presentation at the Global Fintech Fest in September 2023. It is important to remember that these UPI developments are in line with the latest RBI monetary policy announcements.

Apart from the Indian presence in the international payments scene, UPI's acceptability makes overseas payments easier for Indian travellers. UPI payments facility has also been opened up for inbound foreign travellers from the G20 countries.

Mobile number-linked UPI transactions are offered by NPCI in Singapore, Australia, Canada, Hong Kong, Oman, Qatar, USA, UK, Saudi Arabia, and UAE

UPI’s continued growth in India seems like a certainty. UPI is expected to constitute 90% of total retail digital payment volume by the next five years. On the international front, UPI faces giants like Visa and Mastercard who have their grip on 80% of the global payments market. UPI will have to invest heavily in international interoperability infrastructure and technology and also adhere to local compliances and regulations.

UPI’s domestic popularity and international start can act as the wind beneath its wings, as it looks to soar the international skies.

BUY NOW